P&C Industry Statutory Data

Annual, Quarterly, Insurance Expense Exhibit

Every insurer domiciled in the 50 states, the District of Columbia, and U.S. territories such as Guam, Puerto Rico, and the U.S. Virgin Islands must file Statutory Financial Statements. These filings contain a deep set of state‑specific and line‑of‑business‑specific data that provide a clear view into the performance and structure of each state’s insurance marketplace.

Annual statements are generally audited, and unpaid loss reserves are reviewed by an independent actuary, ensuring a high level of reliability. The statements follow standardized formats and reporting rules, allowing consistent comparisons across insurers and states. While the Annual Statement provides the most detail, the Quarterly Statements also contain substantial state‑level and line‑of‑business information that can be used to monitor emerging trends throughout the year. The Insurance Expense Exhibit (IEE) supplement required by the NAIC provides much detail by Lines of Business with expenses like advertising expense allocated.

A.M. Best Financial Suite

Real Insurance Solutions Consulting is a licensed user of A.M. Best’s Financial Suite, which provides access to insurer financial statements, credit ratings, performance ratios, and industry‑level analytics. These data are drawn directly from raw statutory filings and aggregated to produce clear, state‑specific insights focused on what matters most to independent agents.

The analysis emphasizes pre‑reinsurance results, offering a true picture of marketplace activity based on the full volume of policies written, premiums earned, losses paid, loss reserves (including loss adjustment expenses), dividends, and operating expenses. This approach highlights what is actually occurring in each state’s insurance marketplace—across all carriers, all lines, and all business written—before reinsurance arrangements obscure underlying trends.

A distinctive aspect of Real Insurance Solutions Consulting’s methodology is the ability to examine each insurer individually or group insurers by similar distribution styles, creating more meaningful peer comparisons. This also allows analysis at both the policy‑issuing company level and the broader insurance group or fleet level, depending on the question being explored.

Storm Events Data

NOAA/NCEI Storm Events Database

Storm event information is sourced from the NOAA National Centers for Environmental Information (NCEI) Storm Events Database, which contains official National Weather Service records of significant weather events across the United States, including event locations, impacts, and documented property and crop damage.

Like statutory financial data, these records are analyzed and organized to provide a state‑specific view of weather activity from the perspective of the independent agent. A 25‑year history of Storm Events is used to give meaningful context on both frequency and severity. Severity is evaluated using measures such as wind speed, hail size, hurricane category, and reported dollar losses or deaths/injuries for events such as wildfires.

The analysis also incorporates GPS‑based mapping of storm paths within each state, showing both in‑state and cross‑border events along with indicators of severity. One particularly valuable feature is the ability to visualize the start and end points of tornado tracks, providing a clearer understanding of where storms originate, how they move, and which communities are most affected.

Rate/Form/Rule Filing Data

Rate/Form/Rule Filings

Publicly Available Rate, Form, and Rule Filings: Insurers nationwide submit rate, form, and rule filings to state insurance departments to propose changes to insurance products, rating structures, underwriting rules, and policy forms. Most states make these regulatory filings publicly accessible, providing valuable visibility into the marketplace.

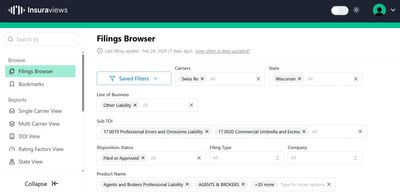

Real Insurance Solutions Consulting accesses this publicly available filing information through Insuraviews, an analytics platform that organizes, structures, and enhances rate and form data for research and marketplace analysis. This system allows filings to be searched, filtered, and aggregated efficiently, making it possible to identify state‑specific trends such as rate movements, product changes, underwriting rule revisions, and insurer regulatory activity. When combined with statutory financial data, these insights can highlight emerging marketplace pressures and potential future premium increases at the state level.

The publicly available data includes insurer submissions, actuarial memoranda, correspondence with regulators, approval dispositions, and historical filing activity. Because filings follow standardized regulatory formats, they can be reviewed consistently across states and lines of business.

Real Insurance Solutions Consulting uses this information to develop state‑specific insights into marketplace activity. By examining rate changes, form revisions, rule updates, and insurer–regulator interactions, the analysis highlights trends that matter to independent agents—such as which carriers are adjusting rates, introducing new products, modifying underwriting rules, or responding to emerging loss pressures. Filings can be reviewed at the individual insurer level or aggregated to show broader patterns within a state’s insurance marketplace.